Provision For Bad Debts / Banks usually provide lots of loans and under ifrs 9, they have to apply general models to calculate impairment loss for loans.

Provision For Bad Debts / Banks usually provide lots of loans and under ifrs 9, they have to apply general models to calculate impairment loss for loans.. Charged to the profit and loss account. If the business expects that some of its customers will fail to pay back the amount that they owe, then the business will create a provision for bad debts or a provision for doubtful debts. Journal entry for bad debts: A bad debt provision is made where there is some reasonable expectation that a trade debtor (s) may not pay their debt, either in part of full. It is done on the reason that the amount of loss is impossible to ascertain until it is proved bad.

The provision for bad debts is an estimate of the debts owed to us that will go bad in the future. For example, they may rent redundant offices and have lease receivables. The bad debt provision account is an accounts receivable contra account, which means that it contains a balance that is the reverse of the normal debit balance found in the associated accounts receivable account. It is similar to the allowance for doubtful accounts. When business firm provides credit facility, in this situation bad debts arise.

Bad Debt Q6 - Estate Agent's Examination Part 1&2 from 3.bp.blogspot.com Businesses usually create a provision for doubtful debt to provide for doubtful debts. The provision for doubtful debts is an estimated amount of bad debts that are likely to arise from the accounts receivable that have been given but not yet collected from the debtors. They are deducted from debtor (account receivable or bills receivable). Next year, the actual amount of bad debts will be debited not to the profit and loss account but to the provision for bad and doubtful debts account which will then stand reduced. While provision for doubtful debts needs to be recorded as an expense in the income statement in the first year of trading. It is done on the reason that the amount of loss is impossible to ascertain until it is proved bad. Bad debts a/c vat a/c sales ledger control account being the write off of a bed debt and claim for bad debt relief 600.00 105.00 705.00 this is the write off of a specific bad debt. As per accounting, bad debts are treated as an expense in the income statement;

When business firm provides credit facility, in this situation bad debts arise.

When business firm provides credit facility, in this situation bad debts arise. Definition of provision for bad debts the provision for bad debts could refer to the balance sheet account also known as the allowance for bad debts, allowance for doubtful accounts, or allowance for uncollectible accounts. For example, let's say that at the end of the year we have $200,000 in debtors control (or accounts receivable). A bad debt provision is created with a debit to the bad debt expense account and a credit to the bad debt provision account. Bad debts a/c vat a/c sales ledger control account being the write off of a bed debt and claim for bad debt relief 600.00 105.00 705.00 this is the write off of a specific bad debt. Under the provision or allowance method of accounting, businesses credit the accounts receivable category on the balance. It is done on the reason that the amount of loss is impossible to ascertain until it is proved bad. Provision for bad debts is deducted after bad debts. Charged to the profit and loss account. When an entity executes transaction of sales on a credit basis it creates and adds on to the amount due from sundry debtors. Provision for bad debt cr the provision for bad debt is estimated each year at the end of the accounting period. Provision for bad debts should be called bad debts allowance by: (4) bad debts and provision for doubtful debts are treated as completely separate items.

Bad debts a/c vat a/c sales ledger control account being the write off of a bed debt and claim for bad debt relief 600.00 105.00 705.00 this is the write off of a specific bad debt. In addition, this accounting process prevents the large swings in operating results when uncollectible accounts are written off directly as bad debt expenses. Charged to the profit and loss account. It is similar to the allowance for doubtful accounts. Provision for doubtful debts are the expected losses of the business, and as per the prudence concept, expected losses are to be treated as expenses.

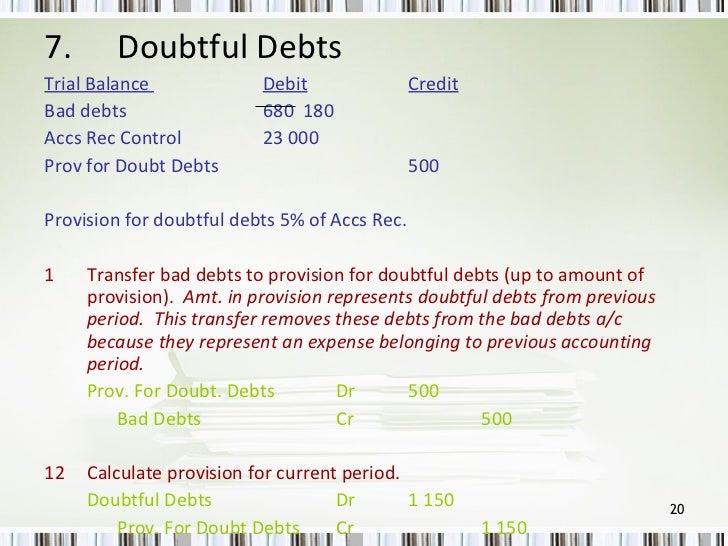

End of period reports from image.slidesharecdn.com Companies have different methods for. An adjustment should be made in the tax computation for any such general provision in the income statement. The provision for bad debts is treated as expense in income statement. The reason for the preference is because the method involves a contra asset account that goes against accounts receivables. The bad debt provision account is an accounts receivable contra account, which means that it contains a balance that is the reverse of the normal debit balance found in the associated accounts receivable account. For example, let's say that at the end of the year we have $200,000 in debtors control (or accounts receivable). Provision for doubtful debts are the expected losses of the business, and as per the prudence concept, expected losses are to be treated as expenses. To provision for bad and doubtful debts.

Next year, the actual amount of bad debts will be debited not to the profit and loss account but to the provision for bad and doubtful debts account which will then stand reduced.

Businesses usually create a provision for doubtful debt to provide for doubtful debts. Definition of provision for bad debts the provision for bad debts could refer to the balance sheet account also known as the allowance for bad debts, allowance for doubtful accounts, or allowance for uncollectible accounts. Provision for bad debts is the estimated percentage of total doubtful debt that needs to be written off during the next year. They are deducted from debtor (account receivable or bills receivable). Next year, the actual amount of bad debts will be debited not to the profit and loss account but to the provision for bad and doubtful debts account which will then stand reduced. 3 general provision for bad debts general provision for bad debts which is based on a percentage of total sales or outstanding debts, is not tax deductible even though the taxpayer may be required to do so under law and accounting convention. Under this method, the company creates an allowance for doubtful accounts, also known as a bad debt reserve, bad debt provision, or some other variation. Provision for both bad debts and discount are to be 5% of the book debt outstanding on the date. The provision for the bad debt is an expense for the business and a charge is made to the income statements through the bad debt expense account. (4) bad debts and provision for doubtful debts are treated as completely separate items. A bad debt provision is made where there is some reasonable expectation that a trade debtor (s) may not pay their debt, either in part of full. The provision is used under accrual basis accounting, so that an expense is recognized for probable bad debts as soon as invoices are issued to customers, rather than waiting several months to find out exactly which invoices turned out to be uncollectible. Provision for doubtful debts are the expected losses of the business, and as per the prudence concept, expected losses are to be treated as expenses.

As per accounting, bad debts are treated as an expense in the income statement; They are deducted from debtor (account receivable or bills receivable). (3) the amounts with which provisions for doubtful debts and discounts allowed decrease are added in gross profit in the income statement as incomes. Provision for bad debts is deducted after bad debts. If so, the account provision for bad debts is a contra asset account (an asset account with a credit balance).

Prepare the bad debts account, provision for account ... from www.sarthaks.com Provision for bad debt cr the provision for bad debt is estimated each year at the end of the accounting period. But occasionally, banks can have other financial assets, too. The provision for bad and doubtful debts will appear in the balance sheet. Anonymous hi i would like to comment on the fact that the word provision as defined by ias 37 restricts provisions to present obligations resulting from past activities of uncertain amount or uncertain timing but for which a reasonable estimate can be made. Businesses usually create a provision for doubtful debt to provide for doubtful debts. The reason for the preference is because the method involves a contra asset account that goes against accounts receivables. It is done on the reason that the amount of loss is impossible to ascertain until it is proved bad. It is nothing but a loss to the company which needs to be charged to the profit and loss account in the form of provision.

Journal entry for bad debts:

The provision for bad and doubtful debts will appear in the balance sheet. They are deducted from debtor (account receivable or bills receivable). This way the matching principle of accounting is followed and no gaap are violated. Bad debts a/c vat a/c sales ledger control account being the write off of a bed debt and claim for bad debt relief 600.00 105.00 705.00 this is the write off of a specific bad debt. Charged to the profit and loss account. When a firm sells goods on credit, there may be bad debts, provision for bad debts and discount on debtor. (4) bad debts and provision for doubtful debts are treated as completely separate items. Provision for doubtful debts are the expected losses of the business, and as per the prudence concept, expected losses are to be treated as expenses. In addition, this accounting process prevents the large swings in operating results when uncollectible accounts are written off directly as bad debt expenses. The balance on the bad debts account at the end of the financial year would be transferred ie: For example, let's say that at the end of the year we have $200,000 in debtors control (or accounts receivable). Provision for bad and doubtful debt is a contra asset i.e it reduces the balance of an asset specifically the receivables. Next year, the actual amount of bad debts will be debited not to the profit and loss account but to the provision for bad and doubtful debts account which will then stand reduced.

Related : Provision For Bad Debts / Banks usually provide lots of loans and under ifrs 9, they have to apply general models to calculate impairment loss for loans..

{kind=link}